Photo voltaic and wind capability within the Affiliation of Southeast Asian Nations (ASEAN) area elevated by 20% in 2023, bringing the entire to greater than 28 gigawatts (GW).

The applied sciences now make up 9% of electrical energy producing capability in ASEAN international locations – Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand and Vietnam – in response to a brand new report from World Power Monitor (GEM).

Mixed with a big base of hydropower, the expansion in wind and photo voltaic takes the bloc near its renewable vitality capability goal of 35% by 2025, GEM says.

Constructing a further 17GW of utility-scale photo voltaic and wind tasks within the subsequent two years – those who feed energy instantly into the electrical energy grid – can be enough to achieve the aim, it provides.

In truth, it says the area is on monitor to sail previous its goal, almost doubling wind and photo voltaic capability within the subsequent two years by including an extra 23GW of latest tasks

An excellent bigger 220GW pipeline of latest utility-scale wind and photo voltaic capability has been introduced, or entered pre-construction or development phases, in response to GEM’s evaluation, although solely 6GW of that is at present being constructed.

Nevertheless, ASEAN international locations collectively have one of many fastest-growing economies on the earth and have seen very speedy latest electrical energy demand development of twenty-two% per yr between 2015 and 2021. This has translated into continued help for gasoline and coal energy within the area, regardless that demand development is predicted to gradual.

Whereas renewables have the potential to mood the expansion in fossil gasoline demand, wind and photo voltaic enlargement face regulatory hurdles and an absence of supportive coverage, GEM provides.

Success up to now

ASEAN added 3GW of photo voltaic capability in 2023, rising put in capability by 17% over 2022 ranges, in response to GEM’s report.

Regardless of photo voltaic seeing a bigger total capability enhance, operational wind capability noticed a bigger comparative rise, rising by 29%, or 2GW, since January 2023.

Offshore wind now accounts for 2GW of the working 9GW of utility-scale wind capability within the area.

Given the technical challenges and related increased prices of offshore wind, that is notably noteworthy, GEM states.

Vietnam has by far essentially the most utility-scale photo voltaic and wind capability of all of the ASEAN nations, as seen within the chart under.

The rise in utility-scale photo voltaic and wind capability over the previous yr has come because of a supportive coverage atmosphere throughout many international locations within the ASEAN area, says GEM.

In 2017, Vietnam deployed a sequence of funding insurance policies designed to convey utility scale-solar tasks into operation, for instance. Two feed-in-tariff (FiT) applications have been deployed by the nation’s state-owned utility between 2017 and 2020.

Nevertheless, when these applications expired, Vietnam didn’t administer a alternative, GEM says. As such, regardless of the nation including 12GW of utility-scale photo voltaic capability between 2019 and 2021, gaps in vitality coverage have began to restrict progress.

Simply 1GW of utility-scale photo voltaic and wind was commissioned in Vietnam in 2022, compared with almost 4GW in 2021.

Thailand and the Philippines at present have the second and third highest utility-scale photo voltaic and wind capability within the area, with 3GW of working capability every.

Thailand is the second largest financial system in ASEAN after Indonesia and has benefitted from being seen as a “low-risk nation”, notes GEM, with few obstacles for funding.

The Philippines, in the meantime, hosts a “streamlined venture bidding system”, which permits for an “unencumbered pipeline of venture improvement”, GEM says. At the moment, round three-quarters of its operational utility-scale photo voltaic and wind capability comes from photo voltaic.

Future development

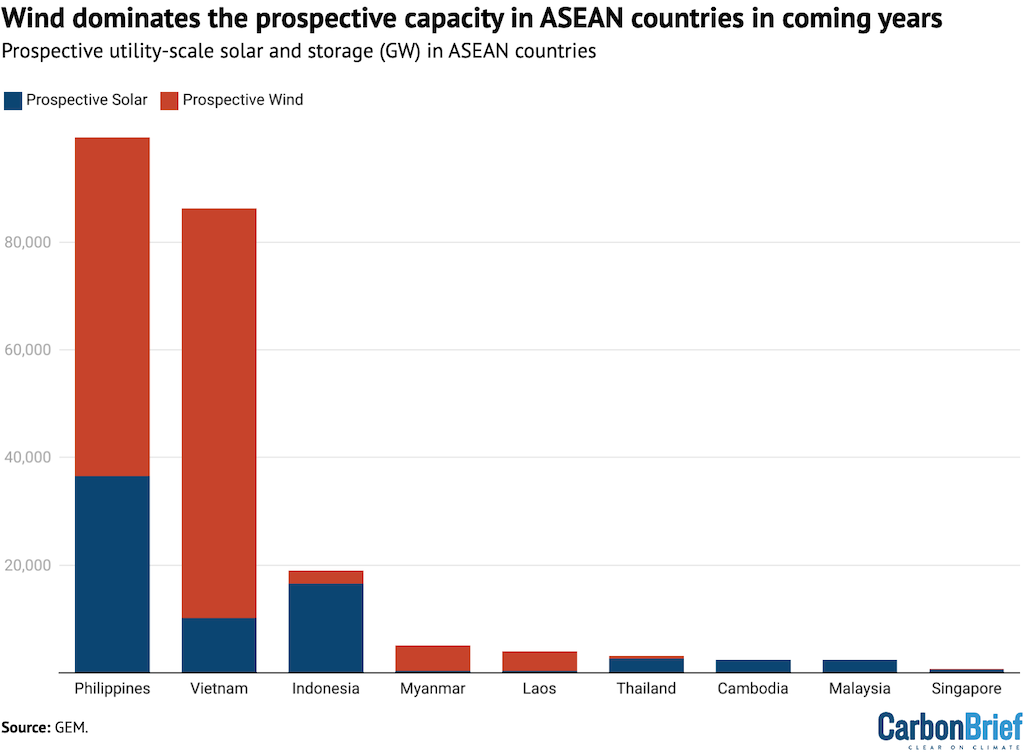

There’s at present a complete of 222GW of introduced, pre-construction and construction-stage utility-scale wind and photo voltaic capability in ASEAN international locations, in response to GEM’s analysis.

Greater than 185GW of this pipeline of tasks is within the Philippines and Vietnam, which means they account for greater than 80% of potential capability within the area. That is proven within the determine under.

Greater than 60% of the pipeline in Vietnam and the Philippines comes from deliberate offshore wind improvement, GEM says, of 72GW and 52GW respectively.

The Philippines is answerable for 45% of potential capability in ASEAN international locations. Its Inexperienced Power Public sale Program (GEAP) goals to facilitate the event of greater than 11GW of renewable vitality.

In March 2023, it held an public sale securing simply over 300 bids to develop 3GW of photo voltaic, onshore wind and bioenergy with 2024–2026 begin dates.

This capability fell wanting the extent focused, however represented a 75% enhance on the quantity secured in 2022’s public sale, notes GEM.

Offshore wind includes 52% of the Philippines’ potential utility-scale renewable capability, with 5 instances extra offshore wind than onshore.

In April 2023, the nation issued an govt order, outlining cooperation between non-public buyers and the federal government on offshore wind. Since then, offshore wind contracts have greater than doubled to almost 80, representing 61GW of capability, GEM notes.

Vietnam has greater than 86GW of potential capability, together with 72GW of offshore wind. Nevertheless, simply 2% is at present being constructed, due partly to the nation’s “lack of concise and dependable renewable vitality insurance policies that would function an important roadmap for venture implementation”, states GEM.

An extra 40GW of utility-scale photo voltaic and wind tasks in Vietnam are thought-about by GEM to be “shelved”, as a result of they’ve seen no development or bulletins previously two years.

Vietnam is engaged on a simply vitality transition partnership (JETP) with a bunch of developed international locations. It additionally launched its newest nationwide electrical energy improvement plan for 2021–2030, often known as the energy improvement plan 8 (PDP8).

The alignment of those insurance policies and funding schemes remains to be in improvement, and subsequently their affect can’t but be decided, notes GEM.

Laos is aiming to “punch above its financial weight” within the improvement of utility-scale photo voltaic and wind capability, GEM says. At greater than 3GW, its potential capability rivals that of Thailand, regardless of the nation’s financial system being solely 2% of the scale.

Laos’ potential utility-scale photo voltaic and wind capability surpasses that of Malaysia by greater than 150%, regardless of having an financial system that’s greater than thirty instances smaller. This ambition is being pushed by monetary collaboration with ASEAN companions, in response to GEM.

Laos is about to deal with the area’s largest onshore windfarm. Monsoon windfarm is at present underneath development and anticipated to have a capability of 600 megawatts (MW) when full.

Regardless of this massive pipeline of ASEAN wind and photo voltaic tasks, nonetheless, solely 6.3GW (3%) is at present underneath development, notes GEM.

Reaching renewable ambitions

The goal for renewables to make up 35% of electrical energy producing capability by 2025 is “simply attainable and in the end unambitious for ASEAN”, in response to GEM.

Renewables already make up 32% of electrical energy capability in ASEAN international locations, GEM says, which means the 35% goal could be met simply.

Furthermore, whereas annual development in electrical energy consumption is predicted to gradual from the annual 22% since 2014 to simply 3% a yr out to 2030, GEM says rising demand will proceed to drive enlargement in fossil gasoline energy infrastructure within the area.

Hitting the 35% goal would solely require ASEAN international locations to fee 17GW of latest renewable capability by 2025, GEM says, of which 6.3GW is already underneath development.

But there may be in extra of 220GW of potential utility-scale photo voltaic and wind in improvement, with a complete of 23GW set to be operational by 2025.

This implies the area is on monitor to beat its goal and almost double its put in wind and photo voltaic capability in simply two years, in response to GEM, with scope to go even additional and cut back the necessity for fossil gasoline enlargement.

For now, fossil fuels stay entrenched within the area, proscribing new funding in utility-scale wind and photo voltaic, GEM states.

Gasoline and coal every account for about 30% of ASEAN international locations’ whole put in capability, and coal-fired energy capability has seen an annual development fee of seven% since 2017.

With electrical energy demand development at present outpacing the rollout of renewable vitality capability, gasoline and coal are anticipated to proceed to develop in coming years, GEM says.

Nationwide vitality insurance policies have touted using gasoline as a “stepping stone” within the vitality transition and ASEAN international locations are more likely to be web importers of gasoline by 2025.

Inadequate grid infrastructure funding can also be a “persistent hurdle” for integrating utility-scale photo voltaic and wind, notes GEM.

As such, whereas there’s a clear effort being made to ramp up renewable vitality, this continues to be sophisticated by a buildout of fossil fuels and low photo voltaic and wind development charges, concludes GEM. The report provides:

“By doubling down on bringing as a lot of the 220GW of potential utility-scale photo voltaic and wind tasks into fruition, ASEAN international locations shall be poised to not solely meet regional renewable vitality targets, however pave the way in which to transition from fossil fuels.”

Sharelines from this story

Discover more from PressNewsAgency

Subscribe to get the latest posts sent to your email.